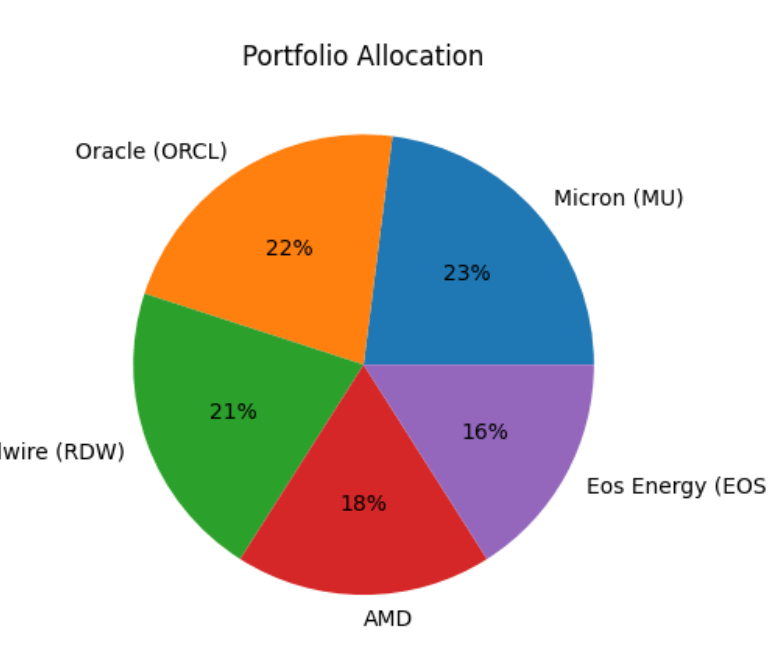

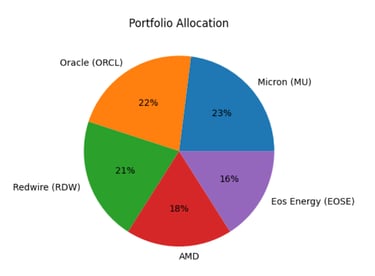

Stock Portfolio - US

Micron Technology (MU)

Micron Technology is one of the world’s largest semiconductor memory manufacturers. The company produces DRAM and NAND flash memory, two critical technologies that power nearly every modern computing system. DRAM acts as a computer’s short-term memory, allowing processors to access data quickly. NAND flash memory stores data permanently in devices like smartphones, servers, and solid-state drives.

The company is headquartered in Boise, Idaho, and is led by CEO Sanjay Mehrotra. Mehrotra previously co-founded SanDisk and has decades of experience in memory technology, making him one of the most knowledgeable executives in the industry.

The semiconductor memory market is extremely difficult to enter because it requires massive capital investments and highly advanced manufacturing processes. Only three companies dominate this sector globally: Samsung, SK Hynix, and Micron. This creates a natural barrier to competition and helps stabilize long-term profitability.

One of the biggest drivers of Micron’s future growth is artificial intelligence. AI systems require enormous amounts of high-bandwidth memory to process large data sets efficiently. New AI data center architectures are pushing memory demand to levels that were unimaginable only a few years ago.

Micron is heavily investing in High Bandwidth Memory (HBM), which is essential for advanced AI accelerators. These memory chips allow GPUs to process massive data streams with extremely high throughput. As AI adoption expands across industries, the demand for HBM is expected to grow dramatically.

The company has also made major progress in manufacturing innovation. Micron continues to advance its DRAM and NAND process technologies, improving density, efficiency, and performance. These improvements allow Micron to reduce production costs while delivering better products.

Another important growth driver is the automotive sector. Modern vehicles require significant computing and memory capacity for autonomous driving, advanced safety systems, and connected infotainment platforms. Electric vehicles and self-driving technologies will likely increase memory usage in cars significantly over the next decade.

Micron also supplies enterprise storage solutions to large data centers. As cloud computing continues expanding, the need for high-performance storage infrastructure will only increase.

Financially, Micron operates in a cyclical industry. Memory prices rise and fall depending on supply and demand conditions. However, the structural growth of AI, cloud computing, and digital services may reduce the severity of these cycles over time.

The company has also benefited from government support through semiconductor investment programs such as the U.S. CHIPS Act. These initiatives aim to strengthen domestic semiconductor manufacturing and reduce geopolitical supply risks.

Micron’s competitive advantage lies in its deep technical expertise and large-scale manufacturing capabilities. Semiconductor memory production is incredibly complex, requiring precision engineering at the nanometer scale.

Over the long term, the growth of digital data, AI workloads, and connected devices will likely keep demand for memory products strong. Micron is positioned as one of the core suppliers of this digital infrastructure.

Oracle (ORCL)

Oracle has been one of the most influential enterprise software companies in the world for decades. Historically, the company built its reputation around database software, which powers the data infrastructure of thousands of large corporations, financial institutions, and government organizations.

Oracle was founded by Larry Ellison, one of the most iconic figures in Silicon Valley. Today, the company is led by CEO Safra Catz, while Ellison continues to play an active role in shaping the company’s long-term technological direction.

For many years Oracle was viewed primarily as a legacy enterprise software provider. However, in recent years the company has undergone a significant transformation by investing heavily in cloud computing infrastructure.

Oracle Cloud Infrastructure (OCI) is now one of the company’s most important growth engines. OCI competes with major cloud providers like Amazon Web Services, Microsoft Azure, and Google Cloud.

Oracle’s strategy is somewhat different from its competitors. Instead of building thousands of smaller data centers, the company focuses on fewer but highly powerful facilities optimized for large-scale enterprise workloads.

One area where Oracle has gained significant momentum is artificial intelligence infrastructure. AI companies require high-performance computing clusters capable of processing massive datasets with minimal latency.

OCI has become an attractive platform for these workloads because of its high-speed networking and efficient data management capabilities. Some AI startups and research groups have already begun using Oracle’s infrastructure for training large models.

Another major advantage for Oracle is its dominant position in enterprise databases. Many organizations rely on Oracle’s database systems to run mission-critical applications. Migrating away from these systems can be extremely difficult and costly.

This creates a powerful form of customer lock-in. Once a company builds its systems on Oracle databases, it often continues using Oracle infrastructure for many years.

Oracle has also expanded its portfolio with enterprise applications such as Fusion ERP and Human Capital Management software. These cloud-based platforms help companies manage finances, supply chains, and workforce operations.

The company’s shift toward subscription-based cloud services has improved the predictability of its revenue streams. Instead of relying primarily on one-time software licenses, Oracle now generates recurring income from long-term service contracts.

Financially, Oracle benefits from very high gross margins typical of software businesses. Once a platform is developed, the cost of delivering software to additional customers is relatively low.

Oracle also generates strong cash flow, which allows the company to reinvest heavily in research, acquisitions, and infrastructure expansion.

One notable acquisition was Cerner, a healthcare information technology company. This move positions Oracle to become a major player in digital healthcare data management.

Overall, Oracle is evolving from a traditional database company into a broader cloud and data infrastructure provider.

Redwire (RDW)

Redwire is a space infrastructure company operating in one of the most exciting emerging sectors of the global economy. The commercial space industry has expanded rapidly in recent years, driven by falling launch costs and increasing private investment.

The company focuses on technologies that support space missions, satellite systems, and orbital manufacturing. Redwire’s CEO is Peter Cannito, who has extensive experience in aerospace and defense industries.

One of Redwire’s most important areas of expertise is space robotics. These robotic systems help assemble, maintain, and operate spacecraft and space stations.

Another key technology developed by Redwire is deployable solar arrays. Satellites rely on solar panels to generate electricity in orbit, and Redwire designs advanced systems that can unfold and deploy once a satellite reaches space.

The satellite economy is growing rapidly. Telecommunications, navigation, weather forecasting, and internet connectivity all depend on satellite infrastructure.

Companies like SpaceX are launching massive satellite constellations. Each satellite requires power systems, sensors, and other components that companies like Redwire help develop.

Redwire is also involved in space manufacturing technologies. Microgravity environments allow certain materials to be produced with unique properties that cannot be replicated on Earth.

This concept could eventually lead to orbital factories producing advanced materials or pharmaceuticals.

Redwire has built its business through a series of strategic acquisitions, bringing together multiple small aerospace technology firms under one organization.

This strategy allows the company to combine expertise from different areas of space engineering.

Although the space economy is still relatively young, analysts believe it could grow dramatically in the coming decades.

Activities such as satellite networks, space tourism, lunar exploration, and orbital manufacturing may become major industries.

Companies that provide infrastructure and hardware for these missions could play a critical role in this ecosystem.

Redwire aims to position itself as one of those enabling companies.

AMD (Advanced Micro Devices)

AMD is one of the most remarkable turnaround stories in the semiconductor industry. For many years the company struggled to compete with Intel in the CPU market.

However, under the leadership of CEO Lisa Su, AMD completely reinvented its technology roadmap and product strategy.

Lisa Su is widely respected in the semiconductor industry for her engineering expertise and disciplined leadership. Her long-term focus on architectural innovation helped AMD regain competitiveness.

The introduction of the Zen processor architecture marked a turning point for the company. AMD’s Ryzen processors quickly became strong competitors to Intel’s chips in both performance and efficiency.

In the data center market, AMD’s EPYC processors gained significant traction among cloud providers and enterprise customers.

Data centers are particularly important because server chips typically have higher profit margins than consumer processors.

AMD is also expanding aggressively into artificial intelligence hardware. The company produces Instinct GPU accelerators designed for AI training and high-performance computing.

Although NVIDIA currently dominates the AI GPU market, AMD is investing heavily to become a viable alternative.

Another strategic move was AMD’s acquisition of Xilinx. Xilinx specializes in FPGA chips, which can be reprogrammed for specialized computing tasks.

These chips are widely used in telecommunications, aerospace systems, and advanced computing applications.

The acquisition significantly broadened AMD’s product portfolio and strengthened its presence in data center infrastructure.

EOSE (Eos Energy)

Eos Energy operates in a completely different part of the technology landscape. Instead of computing hardware or software, the company focuses on energy storage systems designed for electrical grids.

As renewable energy sources like solar and wind expand globally, energy storage becomes increasingly important. Unlike fossil fuel plants, renewable energy production is intermittent.

Solar panels only generate electricity during the day, and wind turbines depend on weather conditions. Without large-scale storage systems, balancing electricity supply and demand becomes difficult.

This is where grid-scale battery technology comes into play.

Eos Energy specializes in zinc-based battery systems designed for long-duration energy storage. These systems are intended to store large amounts of electricity and release it when needed to stabilize power grids.

The company’s CEO is Joe Mastrangelo, who has extensive experience in the energy infrastructure sector.

Most battery technologies currently used in energy storage rely on lithium-ion chemistry. While lithium batteries are widely used in electric vehicles and consumer electronics, they have several limitations for grid applications.

Lithium batteries can be expensive, rely on scarce materials, and pose safety risks such as thermal runaway.

Eos Energy’s zinc battery technology aims to solve these problems. Zinc is abundant, relatively inexpensive, and safer than lithium in large-scale energy storage systems.

The company’s batteries are designed for long operational lifetimes and lower total system costs.

Grid operators around the world are beginning to invest heavily in energy storage infrastructure. As renewable energy capacity increases, the need for large battery systems grows.

These storage systems can smooth fluctuations in electricity supply and reduce strain on power grids.

Energy storage is increasingly viewed as a key component of the global energy transition.

Governments are supporting the development of battery technologies through subsidies and energy transition policies.

Eos Energy is currently scaling up manufacturing capacity to meet expected demand.

While the company is still relatively early in its growth trajectory, the potential market for grid-scale storage is enormous.

Electric grids are some of the largest and most complex infrastructure systems in modern society.

As energy systems become more decentralized and renewable-driven, storage technologies like those developed by Eos could play a critical role.

If the company successfully scales production and continues improving battery performance, it could become an important player in the global energy storage market.